Continuing lack of homecare workers

Findings of fourth Homecare Association member survey on workforce, January 2022

Summary

The Homecare Association conducted a fourth survey of its members on workforce and related issues in January 2022. This followed previous surveys reported in July, August and November 2021. Our aim was to understand how the situation with availability of workforce is developing. Our findings suggest that, despite an easing of some of the pressures that were faced before Christmas, workforce capacity is still inadequate to meet rising demand for homecare.

Responses were received from 296 homecare providers, large and small, state-funded and private-pay funded, in England. Responses were collected between 10 and 24 January 2022.

Key findings were as follows:

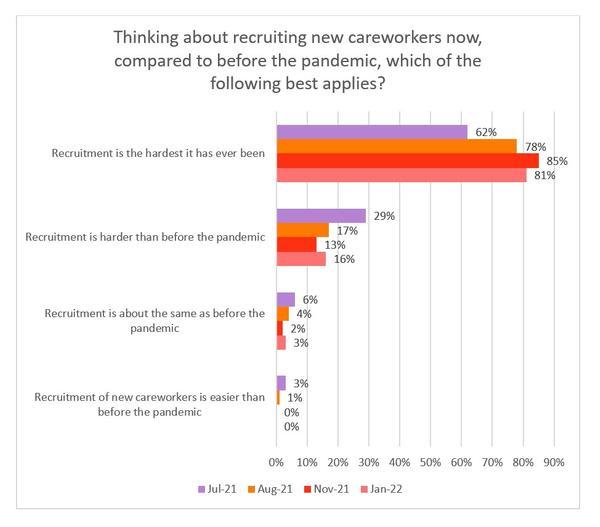

- 97% of homecare providers said that recruitment was harder than before the pandemic, with the majority of respondents (81%) saying that recruitment was “the hardest it has ever been”. The proportion of providers responding with this answer has seemed to peak in November but remains high.

- The majority of care providers (90%) reported that they needed to offer pay rates of £10 or more per hour to attract applicants, with just over a third (34%) offering between £10 and £10.99.

- More than half of respondents (58%) said that they would continue to focus on local recruitment, as opposed to exploring international recruitment with careworkers being added to the Shortage Occupation List.

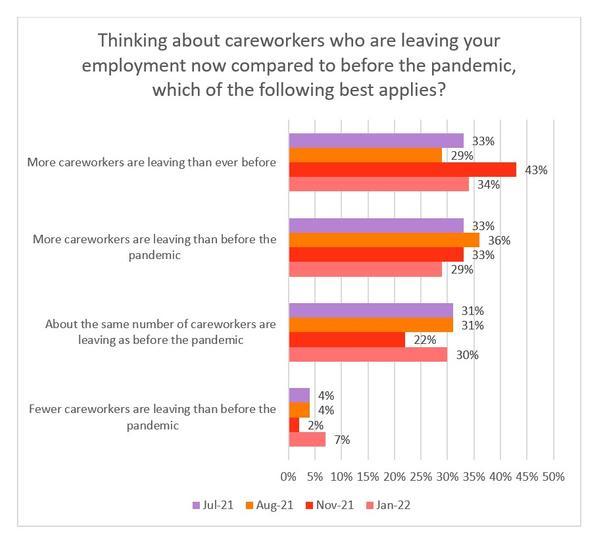

- 63% of homecare providers said that more careworkers were leaving more often than before (compared to 75% in November and 65% in August), including 34% who said that more careworkers were leaving than ever before. 7% said that fewer careworkers were leaving than before the pandemic – the highest such proportion over the iterations of this survey.

- There was a clear difference between the private-pay and state-funded sectors on the number of careworkers leaving their roles, the ability to take on new packages of care and the long-term financial viability of providers, with agencies serving the private-pay market experiencing fewer difficulties than those serving the state-funded market.

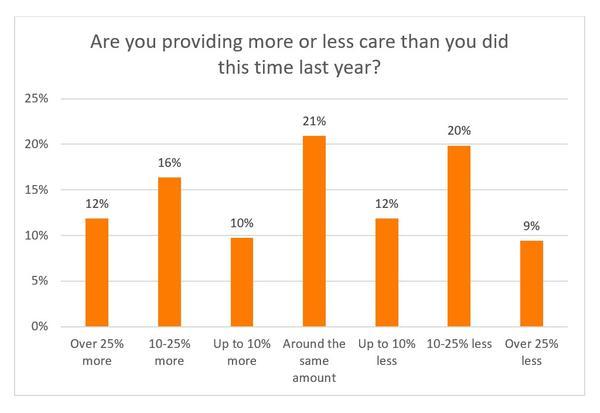

- 91% of providers stated that demand for their services had increased or significantly increased over the previous two months (compared to 93% in November). Just 2% said that demand had reduced or significantly reduced. However, when asked if they were delivering more or less care than this time last year, providers were fairly evenly divided - 38% were providing more than last year, 21% were providing the same amount and 41% were providing less than last year. Differences in volumes of delivery are likely explained by variation in ability to recruit and retain careworkers.

- Careworkers’ pay and available terms and conditions of employment was the greatest challenge to recruiting and retaining homecare workers, with 38% of employers describing that as the most significant issue. Other key factors included competition with other business sectors and staff re-evaluating lifestyle or work/life balance. This is, of course, closely linked to how the homecare sector is funded by the State, and what private individuals arranging their own care are willing and able to pay.

- Only 5% of providers asserted that they should be able to take on most or even all new packages of care that month. However, the percentage of respondents who were expecting not to be able to take on new packages had dropped by 17 percentage points since the last survey in November 2021.

- 25% of providers reported that they were planning to hand some or all of their existing work back to councils or the NHS – a drop of 17 percentage points since November 2021.

- Just under a quarter (24%) of respondents were very concerned about their organisation’s financial viability – a statistic that has fallen by 20 percentage points since the previous survey.

- More than three-fifths (62%) of respondents who are funded by local authorities have yet to hear about fee rates for 2022-23. The responses for those that had heard were varied, with an expected increase of between 2% and 3% being the most common.

- Close to two-thirds of providers (63%) claimed that their staff were either sometimes or usually able to acquire lateral flow tests over the previous four weeks to help facilitate a return to work. At the time of the survey in January 2022, 62% said that availability had now improved, although in most of these cases, problems still existed. (N.B. Due to a subsequent change in policy, availability of LFDs is no longer an issue, though the requirement for daily LFD testing is causing numerous problems).

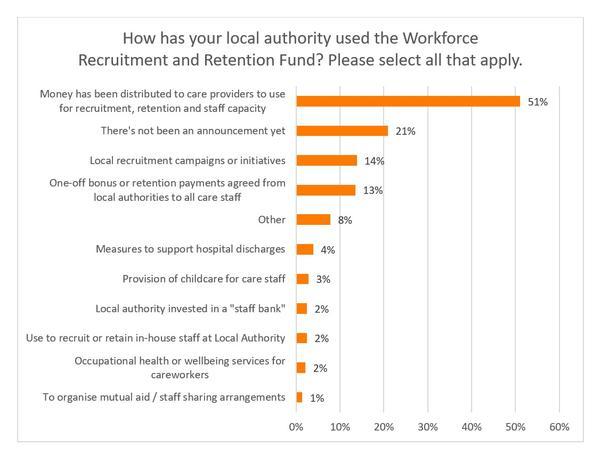

- Over half of respondents (58%) stated that they had not been consulted by their local authority about the use of the Workforce Recruitment and Retention Fund. A further 17% had been consulted but were unimpressed by the quality of the discussions.

- Around half of respondents (51%) mentioned that the money from the Workforce Recruitment and Retention Fund had been allocated to providers for recruitment, retention and staff capacity. Despite this, 21% argued that no announcement on the use of the Fund had been made.

Conclusion

Demand for homecare continues to rise but the number of careworkers available in homecare has reduced. Mismatch between supply and demand in homecare is leading to an increase in unmet need, which risks adversely affecting individuals and their families, as well as the wider health and care system.

The Association of Directors of Adult Social Services (ADASS) reported in November 2021 that almost 400,000 people were waiting for an assessment of their needs or service. More than 1.5 million hours of commissioned home care could not be provided between August and October 2021 because of a lack of staff, despite record growth in provision of 15%. The increase in hours delivered has been achieved with the same or diminishing numbers of careworkers, many of whom are now exhausted.

NHS hospitals are struggling to discharge people back home due to lack of capacity in homecare and other community services, which contributes to ambulance queues, cancelled operations and clinics, and makes it difficult for the NHS to reduce its elective backlog. The NHS has been provided with an additional £1.5 billion for its elective recovery plan, none of which will address workforce issues in social care.

Neither do the much-heralded adult social care reform proposals address long-standing issues with the social care workforce, created by years of central government under-funding. Council budgets have suffered radical cuts, leading to rationing of care and zero-hour commissioning of homecare, at fee rates below those required to ensure quality and sustainability. Careworkers and the people they support have suffered as a result. Zero-hour commissioning of homecare forces zero-hour employment of homecare workers, many of whom are paid by the minute. Pay, terms and conditions of many homecare workers do not reflect the skill and experience needed for these roles and have made retention and recruitment of careworkers very challenging. This needs to change.

The Homecare Association continues to call on the Government to:

- Fund social care adequately so that homecare workers are paid fairly for the skilled roles they perform, and at least on a par with equivalent public sector roles.

- End the practice of councils and the NHS of purchasing homecare “by-the-minute”, alternatively focusing on achieving the outcomes people want.

- Support development of an expert-led workforce strategy for social care and a 10-year workforce plan, aligned with the NHS People Plan.

- Create a professional register for careworkers in England, covering all paid social care workers in both regulated and unregulated care services. Registration of careworkers needs to be adequately funded and carefully implemented.

About the collection method and response rate

Responses were collected through a self-selecting online survey of Homecare Association member organisations between 10 and 24 January 2022. Responses were received from 296 homecare providers, large and small, state-funded and private-pay funded, in England.

In our analysis of answers, we have excluded the very small number of responses stating that they did not know (or preferred not to say) the answer to one or more individual questions.

Organisations completing the survey

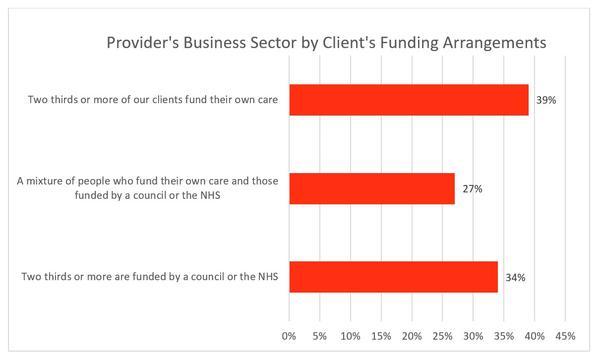

The survey was completed by providers serving either predominantly state-funding or self-funding clients, or a mixture of both. As outlined below, many of these issues are affecting both the state-funded and privately-funded parts of the market but are much more pronounced in those providing state-funded care.

Results

Recruitment of careworkers

97% of homecare providers said that recruitment was harder than before the pandemic, with a majority of respondents (81%) saying that recruitment was “the hardest it has ever been”. The proportion of providers responding with this answer seemed to peak in November but remains high.

Difficulty recruiting careworkers is not confined solely to the state-funded sector, where recruitment of homecare workers is generally regarded as harder than in the private-pay part of the market. Indeed, for those predominantly reliant on self-funders, 79% asserted that recruitment is the hardest it has ever been.

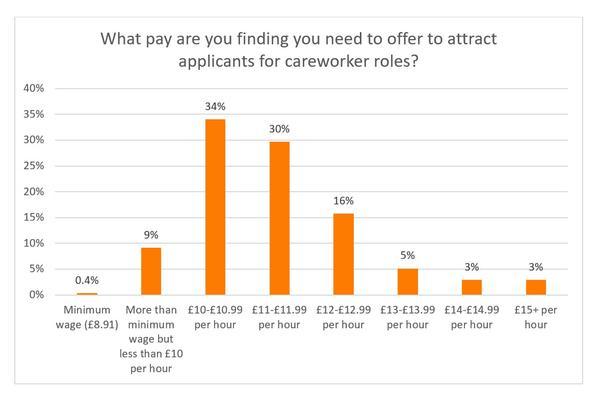

Careworker pay

We asked our members about the rates of pay required to entice applications for careworker jobs. The majority of care providers (90%) said that they needed to offer pay rates of £10 or more per hour to attract applicants, with just over a third (34%) offering between £10 and £10.99. Of those respondents offering at least £15 per hour, who also recorded their location, two were based in the South West, with one each in the North West, West Midlands, South East and East of England.

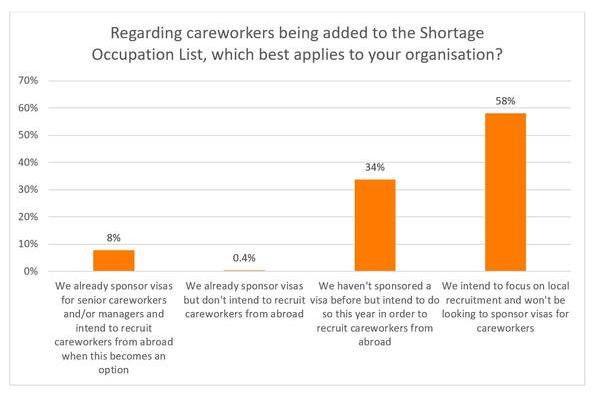

Overseas recruitment

More than half of respondents (58%) said that they would continue to focus on local recruitment, as opposed to exploring international recruitment with careworkers being added to the Shortage Occupation List.

Various reasons were postulated by those not seeking overseas recruitment:

- Cost of sponsorship.

- Unable to meet minimum salary requirement.

- Difficulty in finding affordable accommodation.

- Possible language barriers (as one respondent mentioned, particularly an issue with those receiving care who have dementia or hearing loss).

- Sponsorship process is long and complicated, with some respondents being unsure how to go about it.

- Overseas workers not having a valid driving licence or car.

- Visas are only temporary.

Careworkers leaving their role

63% of homecare providers said that more careworkers were leaving more often than before (compared to 75% in November and 65% in August), including 34% who said that more careworkers were leaving than ever before. 7% said that fewer careworkers were leaving than before the pandemic – the highest such proportion over the iterations of this survey.

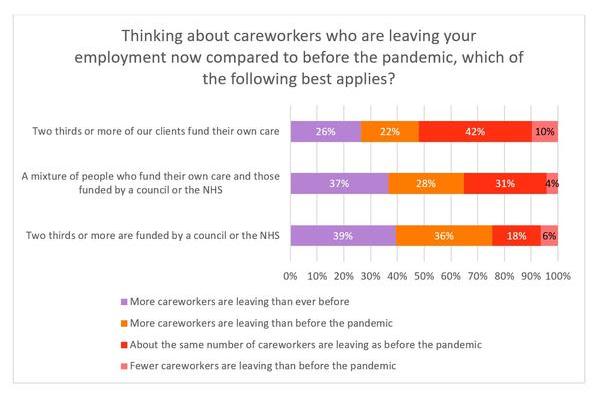

When breaking the data down, there is a clear difference between the private-pay and state-funded sectors. While less than a quarter (24%) who are mostly state-funded have seen fewer or about the same number of careworkers leave, the respective percentage among private-pay providers is 52%.

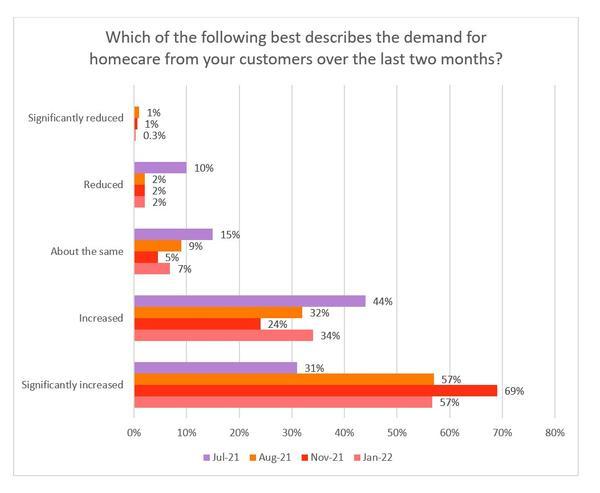

Demand for homecare services

91% of providers stated that demand for their services had increased or significantly increased over the previous two months (compared to 93% in November). Just 2% said that demand had reduced or significantly reduced. [Note, regarding the below graph, there was not a figure for ‘significantly reduced’ in July].

Amount of care

Despite the sharp increase in demand, when asked if they were delivering more or less care than this time last year, providers were fairly evenly divided - 38% were providing more than last year, 21% were providing the same amount and 41% were providing less than last year. This is most likely to be related to ability to recruit and retain staff as demand for homecare appears to be high everywhere.

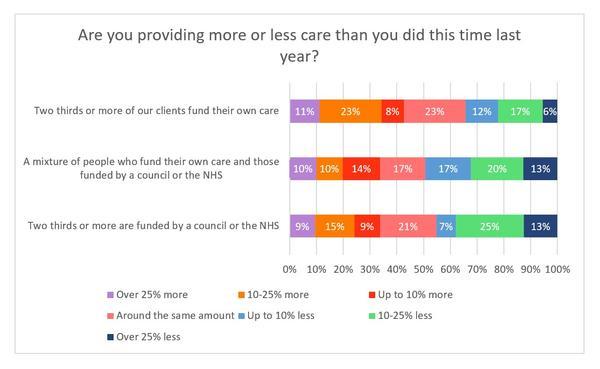

It is also interesting to see that, when splitting the data by type of funding source, the proportion in the private-pay sector who were delivering more care than last year is nine percentage points higher than those in the state-funded sector.

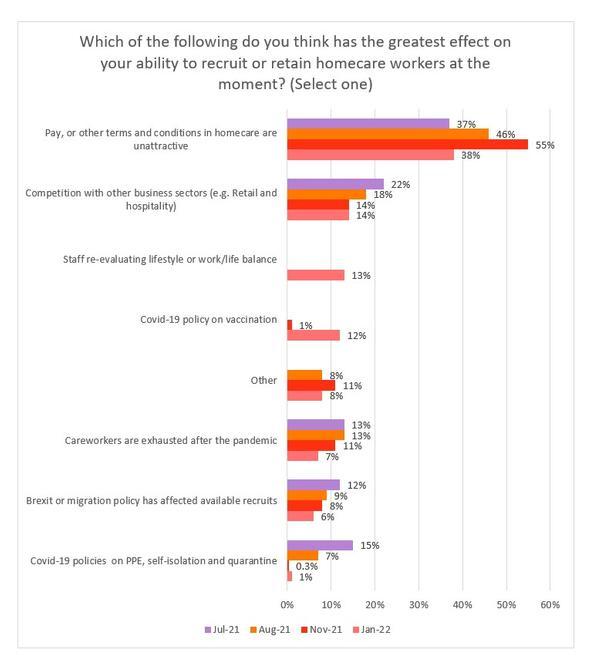

Reasons for challenges in recruitment and retention

Providers reported that the key challenges to recruitment and retention were:

- Pay, terms and conditions of employment.

- Competition with other business sectors.

- Staff re-evaluating lifestyle or work/life balance.

- COVID-19 policy on vaccination.

- Exhaustion and burn-out of careworkers.

Careworkers’ pay and available terms and conditions of employment was the greatest challenge to recruiting and retaining homecare workers, with 38% of employers describing that as the most significant issue.

This is, of course, closely linked to how the homecare sector is funded by the State, and what private individuals arranging their own care are willing and able to pay.

The option ‘Other’ represented a range of views, including:

- Staff leaving or reducing hours due to mental health problems.

- Lack of appreciation of the role that careworkers perform.

- Inability of staff to work more hours due to potential loss of Universal Credit.

- Combination of factors.

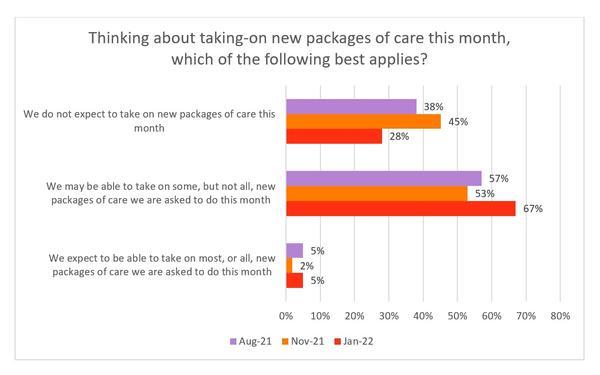

Providers’ assessment of their ability to provide homecare to new clients

Only 5% of providers asserted that they should be able to take on most or even all new packages of care this month. However, the percentage of respondents who are not expecting to take on new packages has dropped by 17 percentage points since the last survey in November.

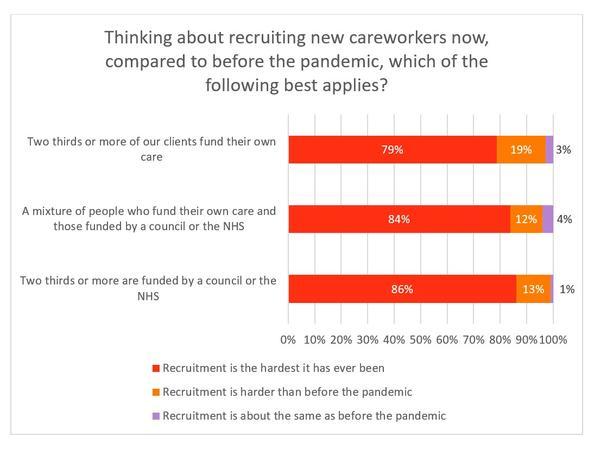

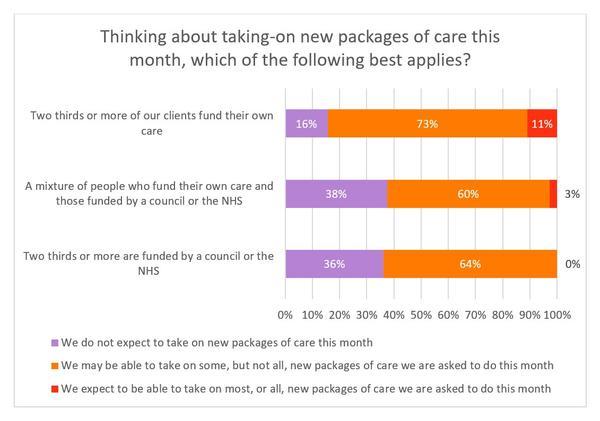

Again, there was a stark contrast between providers who primarily worked with people who funded their own care and those who primarily worked with NHS and local authority commissioned care. Only 16% in the former category were not expecting to take on new packages of care, compared with 36% for the latter. Furthermore, not a single state-funded respondent expressed that they should be able to take on most or all new packages of care.

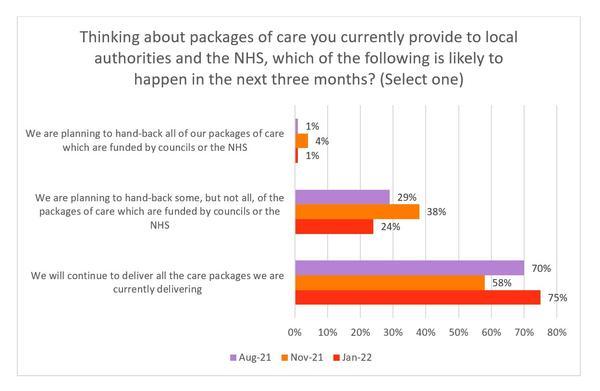

Providers’ assessment of their ability to continue supporting their existing homecare clients

Please note that this question was only asked of homecare providers who delivered services to local councils or the NHS.

25% of providers reported that they are planning to hand some or all of their existing work back to councils or the NHS – a drop of 17 percentage points since November.

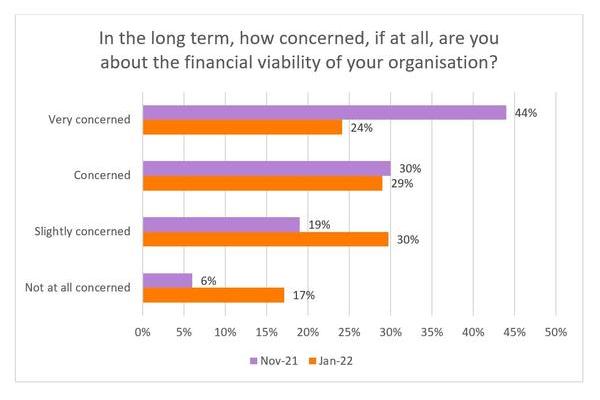

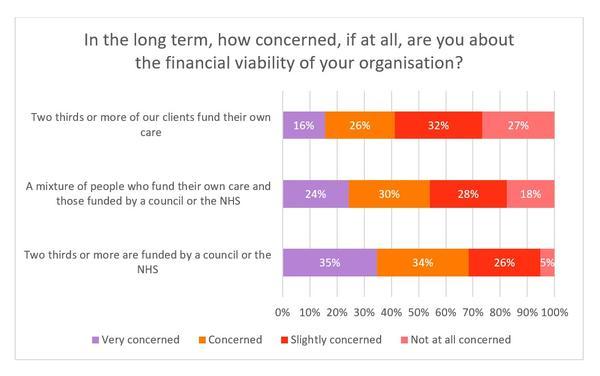

Concerns about long-term financial viability

Just under a quarter (24%) of respondents were very concerned about their organisation’s financial viability – a statistic that has fallen by 20 percentage points since the previous survey.

The level of anxiety was more pronounced among those providing council or NHS-funded care, with more than two-thirds (68%) expressing concern (compared with 41% among those mostly reliant on self-funders).

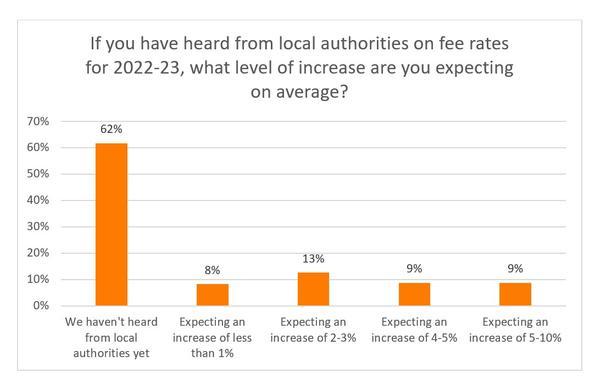

Local authority fee rates

More than three-fifths (62%) of respondents who are funded by local authorities have yet to hear about fee rates for 2022-23. The responses for those that had heard were varied, with an expected increase of between 2% and 3% being the most common.

Booster vaccine hesitancy

The main reasons given for vaccine hesitancy for the booster among staff were:

- Freedom of choice or is not commensurate with personal beliefs (e.g. religious).

- Potential side effects (e.g. alleged impact on fertility) or a question mark over its efficacy.

- Concern of impact on an existing health condition.

- Misinformation on social media.

- Fear of needles.

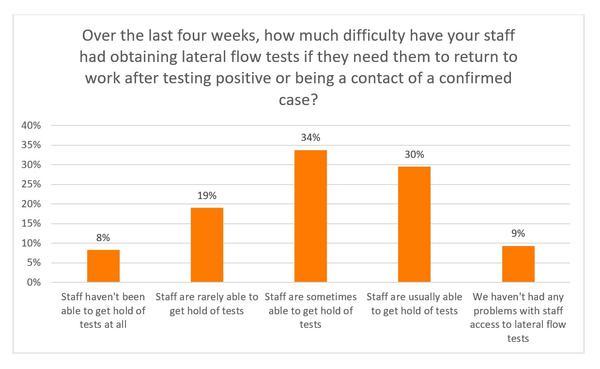

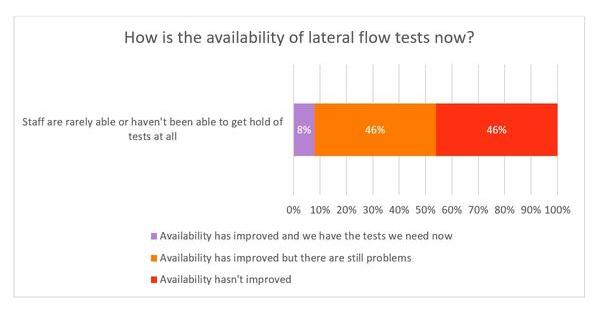

Access to lateral flow tests

Close to two-thirds of providers (63%) claimed that their staff were either sometimes or usually able to acquire lateral flow tests over the previous four weeks to help facilitate a return to work.

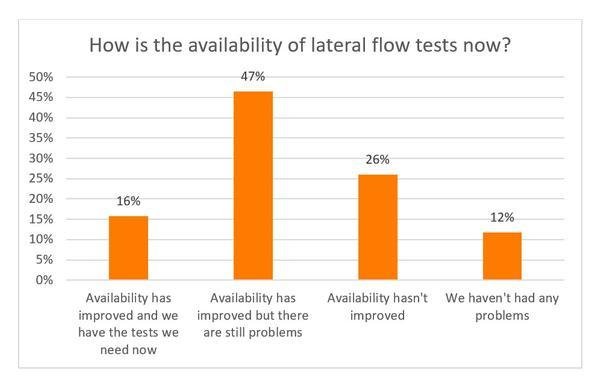

At the time of the survey in January 2022, 62% said that availability had improved, although in most of these cases, problems still existed.

Of the 76 respondents who stated that staff had rarely or not been able to obtain tests over the last four weeks (in answer to the previous question), only 8% asserted that they now had the tests they needed.

Since this survey was conducted, a change in testing policy for adult social care was announced. Now, instead of one weekly PCR test for asymptomatic careworkers, daily LFD tests are required. This has resulted in LFD test kits becoming readily available for homecare providers. The move to daily LFD testing is, however, creating numerous operational and financial difficulties in homecare and has not been welcomed. The rationale for a different testing regime in adult social care compared with the NHS, where only two LFD tests per week are required, is not understood.

Workforce Recruitment and Retention Fund

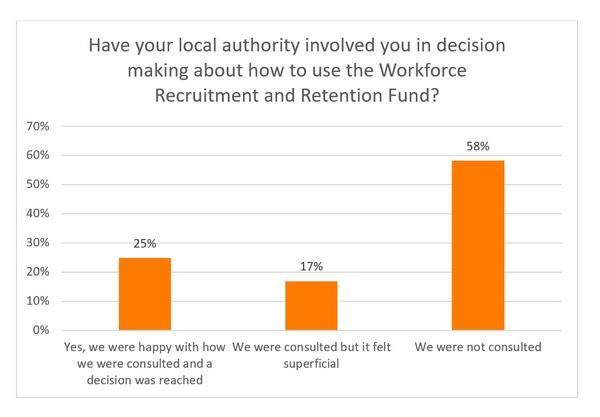

More than half of respondents (58%) stated that they had not been consulted by their local authority about the use of the Workforce Recruitment and Retention Fund. A further 17% had been consulted but were unimpressed with the quality of the discussions.

Around half (51%) mentioned that the money from the Workforce Recruitment and Retention Fund had been allocated to providers for recruitment, retention and staff capacity. Despite this, 21% argued that no announcement on the use of the Fund had been made. Within the ‘Other’ category, responses included:

- Insufficient funding allocated when compared with a neighbouring authority.

- No benefit received due to conditions attached to the funding.

- Money was distributed to framework providers only.

- Majority of the fund to be used for retention (but not recruitment).

- Two providers (one based in the West Midlands, the other in Yorkshire and The Humber) have asked their respective local authority multiple times for information, but not received a response.